The thought of your assets getting tangled in a prolonged legal process — probate — after your demise can be unsettling. While designed to ensure rightful asset distribution, the probate court process often comes with delays, costs, and stress for grieving families.

But it doesn’t have to be that way; avoiding probate is possible when you plan ahead. Dive into an exploration of the probate process, its potential pitfalls, and five strategic ways to bypass its complexities, ensuring a hassle-free asset transfer.

Probate is the formal legal process that includes authentication of a last will and testament (will), the appointment of an executor, and the distribution of assets to intended beneficiaries, either per the will or by state law after a person’s death.

When someone dies with a will, the probate process begins with the appointed executor or personal representative filing the will in court. Under court supervision, the will’s validity is confirmed. Such confirmation gives the executor the authority to handle the deceased’s assets, clear debts, and distribute estate to the listed beneficiaries.

Estates without a will in place undergo probate in accordance with the state’s probate laws. An administrator oversees asset distribution based on a hierarchy: typically, spouse, children, then other relatives. Jointly owned assets transfer to the surviving owner.

If the estate’s outstanding debts exceed assets, probate might not occur.

Typically, there are four types of assets that go through probate:

For smaller estates, many states offer summary probate — a faster, streamlined court process based on the estate’s value. States like Texas even provide informal settlements for estates with only personal property, saving on court, executor, and attorney fees. Check your state’s probate laws to find the property value that may trigger probate.

Avoiding probate is often advisable, and here are four compelling reasons why:

However, if you plan in advance, there are various ways to avoid the probate court system and transfer assets directly to beneficiaries without waiting for your will to be probated.

You can transfer assets without probate if you leave them directly to your heirs or beneficiaries by naming them outside the confines of a will or any order of distributions required by state law. These assets pass automatically at death, ensuring a swift transfer.

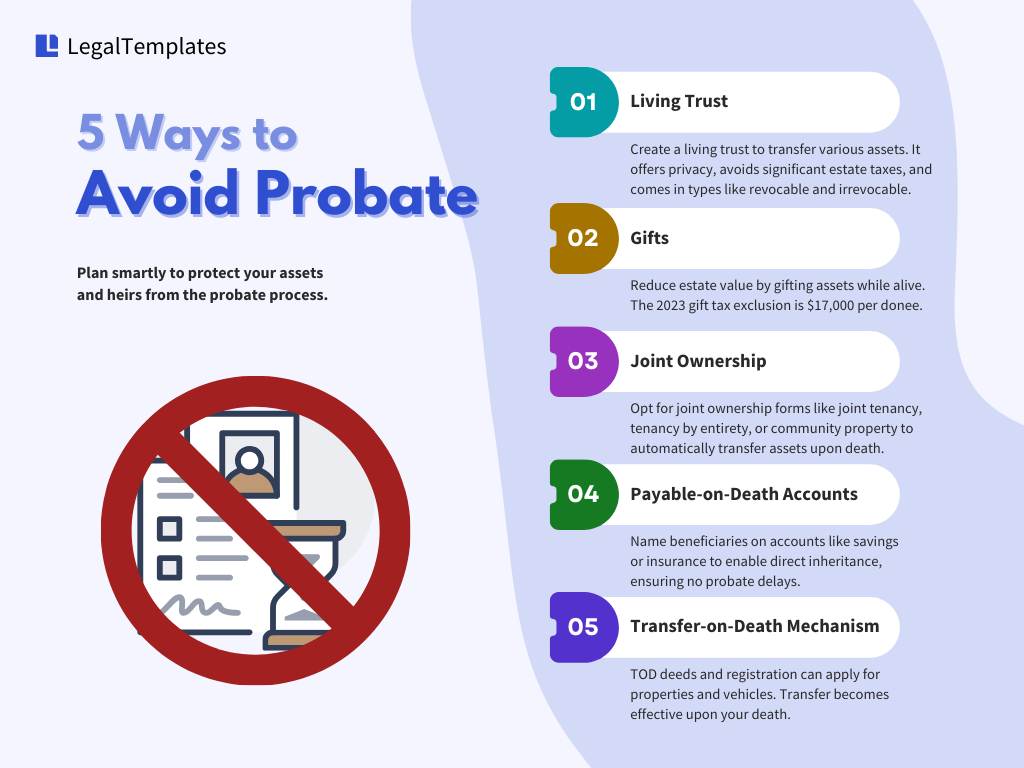

Specifically, here are five clever ways to avoid probate and transfer assets directly:

Complexity Level: High

Suitable for: Various types of assets

By creating a living trust, you establish a separate legal entity to which you can transfer your assets, be it bank accounts, real estate, vehicles, or even unique items like art collections.

Because a living trust is a legal entity set up to hold assets, you can place your assets in a living trust while you’re alive for your beneficiaries to inherit directly after your death. Your appointed trustee will manage and distribute these assets.

Many consider living trusts one of the most efficient methods to transfer property upon death, as they can help you avoid the burden of potentially massive estate taxes. They are also private, meaning that your assets will be distributed in complete privacy.

Different trust types cater to varied needs, and each offers distinct advantages. For instance, revocable living trusts are widely used because they are flexible, can be changed anytime during your lifetime, and can protect your property from probate. An irrevocable trust, however, can offer specific tax advantages.

Complexity Level: Low

Suitable for: Assets of lower values

Gifting assets before death is a proactive strategy to avoid probate. By transferring ownership of assets while you’re alive, assets you no longer own are not part of the probate estate. In addition, you effectively reduce the value of your estate, ensuring fewer assets undergo the probate process upon your death.

In the tax year 2023, the annual gift tax exclusion stands at $17,000 per donee. For example, if you have three children, you can give each of your children $17,000 (or gift assets with values under $17,000 total), and it will be tax-exempt.

While there’s a lifetime limit on the total value of assets you can gift without incurring taxes, there’s no limit to the number of individuals you can gift each year.

The advantages of this approach are apparent: it not only provides an immediate benefit to your loved ones but can strategically decrease your estate value, potentially simplifying any residual probate processes. However, once an asset is gifted, you relinquish all control over it.

Complexity Level: Medium

Suitable for: Assets with titles

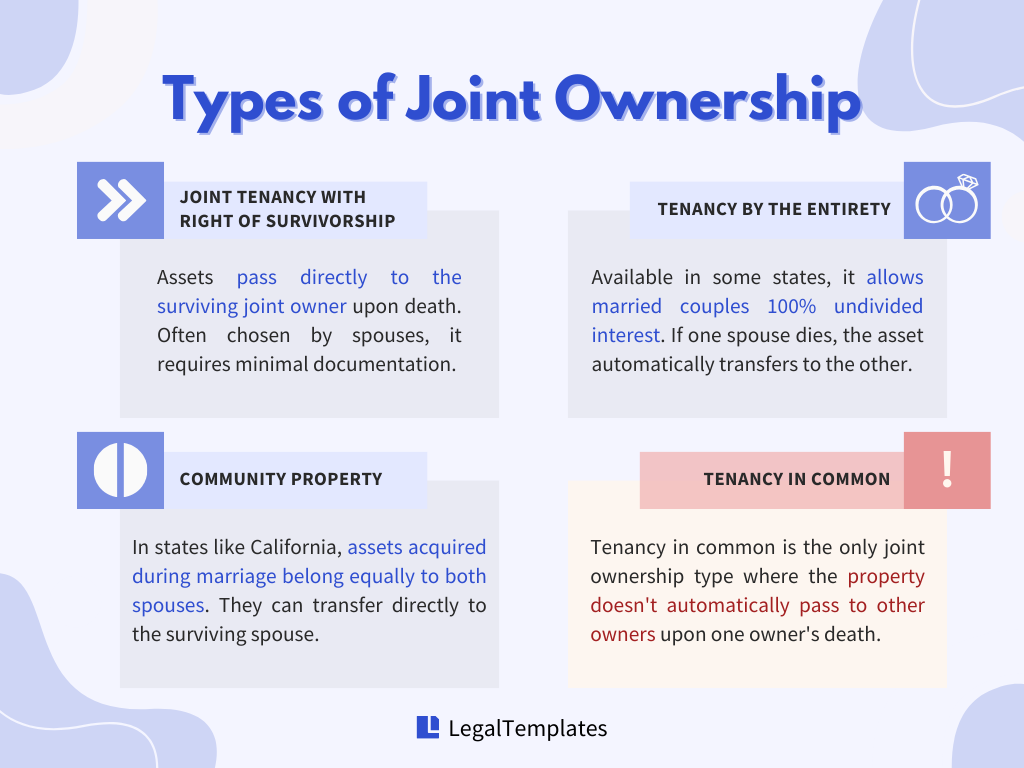

By establishing joint ownership of property with your loved ones, you can have the ownership automatically transferred to them upon your death without the need for probate intervention. Many types of joint ownership can achieve this, including:

This means that when one owner dies, the asset directly passes to the surviving joint owner, avoiding probate. It’s common for spouses to become joint tenants, particularly because it often requires no added documentation other than indicating this type of tenancy on the deed.

This type of ownership is available in about half the states. For married couples only, tenancy by the entirety allows both spouses to have an equal and undivided 100% interest in a property. If one spouse dies, the property automatically belongs to the surviving spouse, ensuring probate stays out of the picture.

In community property states like California, assets acquired by either spouse during the marriage, be it income, real estate, or other properties, belong equally to both spouses. Properties held as community property can pass directly to the surviving spouse, sidestepping the probate process.

Despite its advantages, joint ownership also has its pitfalls. It can complicate matters if relationships sour or if one owner incurs debt, as the asset might be at risk.

Tenancy in common, where two or more people have ownership interest, is the only type of joint ownership that does not allow the property to be passed directly to other owners if one owner dies.

Complexity Level: Low

Suitable for: Financial accounts, life insurance policies, pension funds, retirement accounts, 401(k) accounts

Payable-on-death (POD) accounts do exactly what the name entails: they pay on death. They let you name beneficiaries who inherit the funds directly upon your death without waiting for letters testamentary or other probate procedures.

POD accounts are particularly helpful when your named executor is also the beneficiary on the POD account. Usually, upon death, a bank will freeze an individual’s account. To access the funds, the executor typically needs to present a death certificate or letters of testamentary issued by the court. With a POD account, these delays are circumvented, and the beneficiary gets immediate access.

Similar to POD accounts, assets like life insurance policy proceeds, funds in pension, or retirement plans can also bypass probate with beneficiary designation. These designated beneficiaries have no rights to the assets until the account holder’s death. This means you maintain complete control during your lifetime and can spend, invest, or change the beneficiary as you see fit.

Always ensure that your beneficiary information is up-to-date, especially after significant life events such as marriage, divorce, or the birth of a child, to prevent unintended inheritance disputes or complications.

Complexity Level: Low

Suitable for: Motor vehicles, real estate properties

The transfer-on-death (TOD) mechanism is comparable to POD accounts since it only takes effect upon your death, and you have the right to manage the assets however you please during your lifetime.

A TOD deed, sometimes known as a beneficiary deed, is particularly useful for transferring real estate. Unlike standard property deeds, a TOD deed doesn’t take effect until your death. However, not all states recognize this arrangement, so check whether your state allows for TOD deeds.

Beyond real estate, the Uniform Transfer on Death Securities Registration Act permits individuals to designate beneficiaries for various financial instruments, including stocks, bonds, and brokerage accounts. Like TOD deeds for properties, these registrations grant you complete control over the assets while you are alive, allowing you to manage, sell, or modify them at will.

For vehicle owners, many states allow the use of TOD forms to transfer the title of cars or other vehicles seamlessly. The designated beneficiary usually needs the vehicle’s title and the original death certificate to process the title transfer.

Review and update your TOD designations regularly. Life changes, such as the birth of a new family member, marriage, or divorce, might necessitate adjustments to ensure your assets go to the intended beneficiaries.

Understanding how to avoid probate is crucial in estate planning, as the probate process can be lengthy and burdensome for beneficiaries. By exploring various ways to avoid probate, such as using living trusts, joint ownership, or POD accounts, you can ensure a smoother transition of assets to loved ones.

Join over 500,000 users who planned ahead with us by creating your estate plan now.

A will in and of itself does not bypass the probate process. In fact, a will is usually the main document presented during probate to guide the distribution of assets. However, a meticulously drafted will can simplify and expedite the process by clearly delineating the testator’s intentions.

Yes. As previously mentioned, there are several ways to transfer property without involving the probate court. Some include setting up living trusts, co-owning assets that allow assets to pass to the surviving owner(s) automatically, and creating transfer-on-death deeds to enable direct transfer of assets like real estate or vehicles upon the death of the owner.

The threshold varies from state to state and even from year to year.

For instance, a Californian’s estate may not have to go through probate if they passed away before April 1, 2022 with an estate worth less than $166,250. If, however, the Californian passed after April 1, 2022, the threshold becomes $184,500. On the other hand, Texas’s estate value threshold is at $75,000 (excluding homestead and exempt property).

For the most accurate threshold and exceptions, check your state laws carefully and consult a probate attorney.

PR & Communications Specialist

Raina Chou creates data-driven articles about the most pressing legal issues in the U.S., combining legal insights with a sharp understanding of users’ needs.

Use our living trust form to transfer your estate without probate.